Mastering the CEO Mindset

Financial advisors desire for independence and having more control as to the development of their own differentiated businesses has been growing steadily and creating a very dynamic industry landscape. This transition is also spawning a rapid evolution in financial services from being a financial sales-driven activity into a diversified wealth management profession.

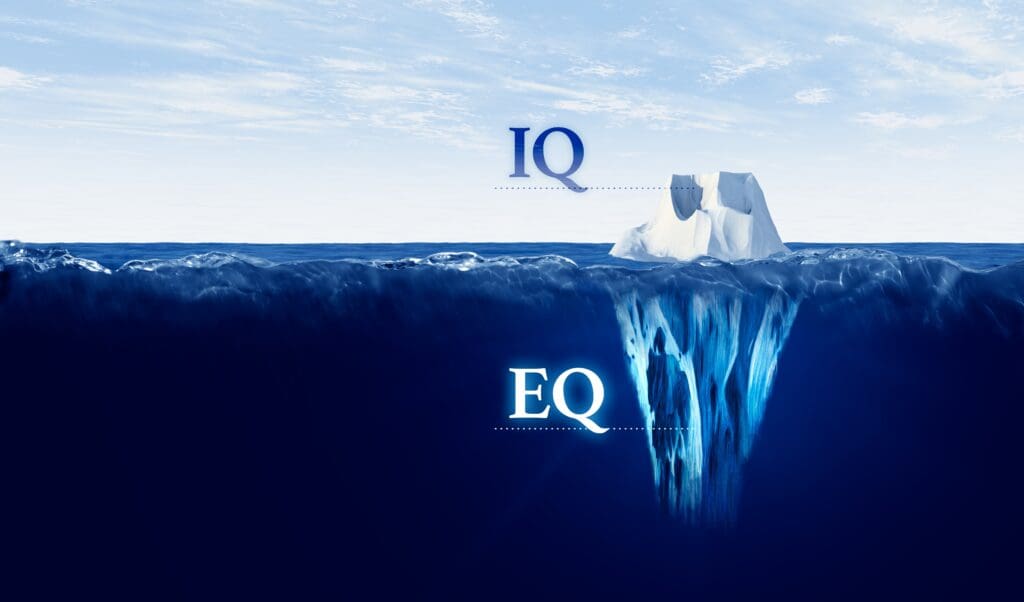

The Power of Emotional Intelligence: How EQ Sets Financial Advisors Apart

Financial advising is not just about numbers and data; it’s also about understanding and connecting with your clients emotionally. The ability to navigate and manage emotions, both yours and your client’s, plays a crucial role in the long-term success of your relationships. This is where Emotional Intelligence (EQ) comes into play.

Boomers to Zoomers: Customizing Financial Strategies Across Generations

In the ever-evolving landscape of wealth management, meeting your clients’ diverse needs means adapting — and dancing to the beat of their generation. When customizing strategies that cater to all clients from tech-savvy Gen Z to the sustainability-minded Gen X and skeptical Millennials (Gen Y) to retiring Baby Boomers, it’s important to have a deeper understanding of their different financial goals, aspirations, and apprehensions.

The Sowell Way— A Modern Turnkey Strategy for Independent Advisors

Financial advisors desire for independence and having more control as to the development of their own differentiated businesses has been growing steadily and creating a very dynamic industry landscape. This transition is also spawning a rapid evolution in financial services from being a financial sales-driven activity into a diversified wealth management profession.

Sowell Management Unveils Latest Strategic Move

“Our long-term roadmap has always included a comprehensive insurance platform,” said founder and CEO Bill Sowell. “This month that became a reality with the launch of Sowell Insurance Services, which includes access to life insurance, annuities, long-term care and disability insurance.”

Safeguarding Your Legacy: Contingency Planning for Independent Financial Advisors

Successful advisors must have a strategic vision to ensure the financial well-being of their clients and safeguard their personal legacy by preparing for unforeseen events that could impact the continuity of their business. ☑️ FREE CHECKLIST ☑️

Sowell Management Named Top Three Fee-Based RIA Firm in the Country

What is your secret to success?

It comes down to two key things: hiring the right people and creating a growth work culture.

The Crucial Partnership: Why Financial Advisors Should Work with Estate Planning Attorneys

One crucial partnership that every financial advisor should consider is working with an estate planning attorney. The collaboration between financial advisors and estate planning attorneys can significantly benefit clients, ensuring their financial well-being and legacy. ✅ FREE CHECKLIST! ✅

Bill Sowell Named 2024 Influencer by AMP

What is your secret to success?

It comes down to two key things: hiring the right people and creating a growth work culture.

Five Outsourced Investment Management Myths Debunked

Investment management outsourcing can be a sensitive topic among financial advisors. While some consider it a risk, others consider it a beneficial strategy to enhance their business. Regardless of where you stand, it’s important for you to clearly understand what outsourcing involves, what the myths and misconceptions are, and what the real benefits are. This blog post will look at some of the most common myths around outsourced investment management and serve as a guide to help you cut through the noise.