We will take the meager stock market gain. While the markets are more reactive to headlines nowadays, Sowell’s technical signals remain steady, fully invested.

A Tug-of-War Between Economic Headwinds and Tech Dominance

This week, the U.S. broad markets ended with a whimper, not a bang, as the S&P 500 managed a meager 0.37% gain. It was a week that felt less like a steady climb and more like a high-wire act, with the market precariously balanced between gloomy economic indicators and the sheer brute force of a handful of mega-cap tech companies. The narrative was crystal clear: investors have stopped caring about the broader economy and are now laser-focused on company-specific catalysts, driven by the growing conviction that a softening labor market will finally prompt the Fed's hand on rate cuts.

The real showstoppers were Alphabet (GOOGL) and Broadcom (AVGO). Alphabet jumped a whopping 10.4% after a federal court handed down a surprisingly favorable ruling in its long-running antitrust case. The verdict, which essentially told the company, "You can keep your Chrome browser, but you have to share your toys," was seen as a massive sigh of relief. It lifted a major legal cloud, allowing the company to get back to the business of, well, everything.

Not to be outdone, Broadcom's stock soared by 12.6% on the heels of a blockbuster earnings report and an even more monumental announcement. The company revealed a landmark partnership with OpenAI to design and create custom AI chips, with initial shipments set to begin in 2026. This news not only topped analyst estimates but also cemented Broadcom's position as a heavyweight contender in the AI hardware race, giving the entire semiconductor sector a moment of glorious, albeit fleeting, excitement.

The fleeting nature of that excitement was made painfully clear by the rest of the semiconductor industry. The PHLX Semiconductor Sector Index fell by 1.57% for the week, not because of a fundamental flaw in technology, but due to a familiar, and frankly, exasperating political headwind. President Trump returned to his "America First" playbook, threatening "substantial" import tariffs on chipmakers that don't shift production to the U.S. This isn't just a tariff threat; it's a direct shot across the bow of a globally interconnected supply chain. Companies like NVIDIA, which fell 4.11%, are particularly vulnerable because their business model relies on a complex web of international manufacturing, from chip design in the U.S. to fabrication in Taiwan. The markets are reacting not to a business problem, but to the unpredictable risk of trade policy, which can disrupt global operations and squeeze profit margins at a moment's notice. It's a classic case of political uncertainty trumping technological innovation.

The relentless growth of the technology sector has now elevated nine out of the top 10 companies in the S&P 500 to a market capitalization exceeding $1 trillion. This elite group, which still includes the ever-present Berkshire Hathaway, now commands a collective market value of over $22 trillion. This extraordinary concentration of wealth and influence is a stark reminder that while a rising tide lifts all boats, some boats are now private yachts with their own helipads.

In the fixed-income market, the 30-year Treasury yield fell by a dramatic 14 basis points to 4.78%. This was the market's way of saying, "We're convinced a rate cut is coming," after a series of underwhelming jobs reports. Curiously, while Treasury yields plunged, 30-year mortgage rates remained stubborn and high, still hovering around 6.64%, offering little relief to a frozen housing market that's just trying to defrost.

On the economic front,

Construction Spending for July fell 0.1% again for the 5th consecutive month, a sign of economic uncertainty and the impact of high interest rates.

ISM Mfg. Employment also trended lower than expected to 43.8, versus the forecast of 45.

July Factory Orders fell by 1.3%, but were in line with expectations.

JOLTS Job Openings survey dropped to 7.18 million, the lowest in 2025, and down from a peak of 11.85 million in March 2022.

Initial Jobless claims rose by another 6,000 to 237k, the highest since June.

What stood out last week was the Nonfarm payrolls report, which showed only 22k jobs created, as wholesale trade and manufacturing both saw declines of 12,000 jobs on the month, well below the forecast of 75k, the lowest level since November 2024. Meanwhile, unemployment rose to 4.3%, the highest level since 2021.

But there was an uptick in job participation rate to 62.3%, generally favorable, but too early to tell heading into the fall holiday season, or is that a sign of rising unemployment?

Looking ahead, market anticipation of a rate cut is expected to reach a fever pitch. With the Fed’s next FOMC meeting looming on September 16th, every data point will be dissected with surgical precision. The spotlight will fall squarely on this week's key inflation reports, with the Producer Price Index (PPI) due on Wednesday, September 10th, and the more widely watched Consumer Price Index (CPI) following on Thursday, September 11th. While the core second-quarter earnings season has concluded, the AI narrative is far from over. All eyes will be on two tech titans this coming week. Oracle (ORCL) is set to report on Tuesday, September 9th, with investors looking for continued momentum in its cloud infrastructure and AI initiatives. Meanwhile, Adobe (ADBE) is scheduled to release its results on Thursday, September 11th, and the market will be eager to see if its AI-powered features can stave off competitive threats and drive meaningful revenue. These releases will provide a crucial glimpse into whether the AI disruption is a fleeting trend or a fundamental shift in the software landscape.

“Something weird has happened about people’s view of the country and the economy. Theres’ a way to predict how people view the economy based on economic statistics. And up until Covid, the statistics and the consumer sentiment rose and fall together. After Covid, they’re totally diverged. The economic statistics look pretty good, but the people’s view of the economy is cratering. And that’s just a generalized loss of faith, the growth of pessimism.”

– New York Times Columnist David Brooks, PBS NewsHour, September 5th, 2025

Defying Trade War Anxiety, EM Stocks Outperform in 2025

Author: Phil Wool, PhD, Chief Research Officer and Head of Portfolio Management at Rayliant

“So far, global trade growth has been highly resilient, and we’ve also not seen all that much retaliation from countries hit by US tariffs. That’s partly because those countries recognize how much they benefit from trade.” —Steven Altman, senior research scholar at the NYU Stern School of Business

With the S&P 500 Index on a year-to-date rally of some 10.4% through the end of August—an undeniably solid return through the first two-thirds of the year—it’s no surprise that many US investors have been fixated on the performance of domestic equities. We imagine that many of the same investors would find it quite surprising to learn that, so far in 2025, the MSCI Emerging Markets Index has more than doubled its performance, gaining over 22% during the same period. So, what explains the outperformance of emerging markets in a year full of the sort of macro uncertainty that usually spells trouble for stocks in developing economies?

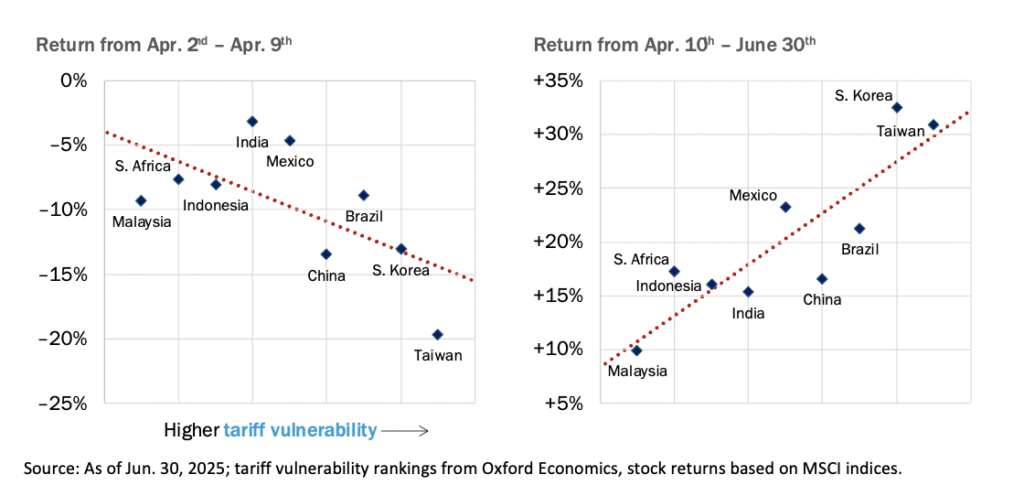

First, let’s consider tariffs, which were a clear headwind to EM stocks at the beginning of the second quarter. The folks at Oxford Economics produced some fascinating analysis of the performance of emerging markets in the wake of Washington’s “Liberation Day” trade tax announcements at the start of April. First, they sorted countries around the world by their estimated economic exposure to US tariffs, then they examined stock returns in the immediate aftermath of April 2nd. Below, we’ve pulled out just the emerging markets, and it’s obvious to us that in the face of intense fear over new trade barriers, markets showing the most US trade policy risk also tended to experience the biggest selloffs.

Bigger Q2 Rebound for Emerging Markets with Higher Tariff Exposure

Tariff vulnerability ranking vs. equity market total return for nine emerging markets

What’s really interesting, though, is what happens in subsequent days, as markets process not only the initial trade threats, but also Washington’s follow-up dealmaking with its biggest trading partners. As huge levies were delayed, initial deadlines extended (then re-extended), and a number of deals announced (never mind the lack of details), markets inevitably discounted those massive “headline” tariffs, leading to a rebound that, symmetrically, tended to be greatest for the markets most exposed to a downturn in trade with the US. The upshot? Investors buying the dip in stocks stung by overly negative sentiment over fears of an all-out trade war—including those in some of the largest emerging markets—turned out to be big winners as the second quarter played out.

But it’s not just the ebb and flow of traders’ sentiment that’s been driving EM stocks to big gains in 2025. There are also fundamental factors at play, which perhaps bode well for the continuation of EM equity strength as the second half proceeds. We think that’s easy to see looking at consensus earnings growth expectations, which have risen to more than 15% annualized over the next two years for the MSCI EM Index since April’s tariff turmoil, compared with projections that have fallen for developed markets in the MSCI World Index, showing roughly 8% growth per annum over the same period.

In part, this we believe divergence reflects the reality of global trade: While we typically think of emerging markets like China as being most exposed to US supply chains, the fact we have found many of the biggest EM firms don’t rely too much on sales to the US—they’ve got growing domestic consumption and exports to the rest of the world to tide them over—while companies in developed economies like Japan and Europe are often heavily dependent on US demand to drive growth. The kicker comes when one examines valuations: Despite expectations for nearly double the EPS growth in the coming years, MSCI EM stocks currently trade at a forward P/E of just 14x, compared to a multiple of over 21x for the MSCI World Index and a lofty 31x for the tech-heavy US NASDAQ composite.

Is there one more potential catalyst for further EM outperformance? The upcoming September FOMC. Some of the worst macro conditions for EM equities historically have been rising US rates and a strengthening dollar. In other words, just the conditions that have prevailed since pandemic-era inflation and the latest cycle of Fed tightening. With the US central bank under severe pressure to ease from the White House, tamer-than-expected inflation, and a softening labor market, traders put the probability of a September cut at 87%, with another four cuts priced in to occur over the next year—plenty of reason for investors to feel good about the future for EM stocks.

Disclosure: This material is for informational purposes only and should not be considered investment advice. The opinions contained herein are subject to change without notice. Indices cannot be invested in directly and are unmanaged.

Advisory services offered through Sowell Management, a Registered Investment Advisor. The views expressed represent the opinion of Sowell Management. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and non-proprietary sources that have not been independently verified for accuracy or completeness. While Sowell Management believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sowell Management’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. International investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles, or from economic or political instability in other nations. Past performance is not indicative of future results.

WEEK AHEAD

September 8-12, 2025

Defying Trade War Anxiety, EM Stocks Outperform in 2025

Author: Phil Wool, PhD, Chief Research Officer and Head of Portfolio Management at Rayliant

“So far, global trade growth has been highly resilient, and we’ve also not seen all that much retaliation from countries hit by US tariffs. That’s partly because those countries recognize how much they benefit from trade.”

—Steven Altman, senior research scholar at the NYU Stern School of Business

With the S&P 500 Index on a year-to-date rally of some 10.4% through the end of August—an undeniably solid return through the first two-thirds of the year—it’s no surprise that many US investors have been fixated on the performance of domestic equities. We imagine that many of the same investors would find it quite surprising to learn that, so far in 2025, the MSCI Emerging Markets Index has more than doubled its performance, gaining over 22% during the same period. So, what explains the outperformance of emerging markets in a year full of the sort of macro uncertainty that usually spells trouble for stocks in developing economies?

First, let’s consider tariffs, which were a clear headwind to EM stocks at the beginning of the second quarter. The folks at Oxford Economics produced some fascinating analysis of the performance of emerging markets in the wake of Washington’s “Liberation Day” trade tax announcements at the start of April. First, they sorted countries around the world by their estimated economic exposure to US tariffs, then they examined stock returns in the immediate aftermath of April 2nd. Below, we’ve pulled out just the emerging markets, and it’s obvious to us that in the face of intense fear over new trade barriers, markets showing the most US trade policy risk also tended to experience the biggest selloffs.

Bigger Q2 Rebound for Emerging Markets with Higher Tariff Exposure

Tariff vulnerability ranking vs. equity market total return for nine emerging markets

What’s really interesting, though, is what happens in subsequent days, as markets process not only the initial trade threats, but also Washington’s follow-up dealmaking with its biggest trading partners. As huge levies were delayed, initial deadlines extended (then re-extended), and a number of deals announced (never mind the lack of details), markets inevitably discounted those massive “headline” tariffs, leading to a rebound that, symmetrically, tended to be greatest for the markets most exposed to a downturn in trade with the US. The upshot? Investors buying the dip in stocks stung by overly negative sentiment over fears of an all-out trade war—including those in some of the largest emerging markets—turned out to be big winners as the second quarter played out.

But it’s not just the ebb and flow of traders’ sentiment that’s been driving EM stocks to big gains in 2025. There are also fundamental factors at play, which perhaps bode well for the continuation of EM equity strength as the second half proceeds. We think that’s easy to see looking at consensus earnings growth expectations, which have risen to more than 15% annualized over the next two years for the MSCI EM Index since April’s tariff turmoil, compared with projections that have fallen for developed markets in the MSCI World Index, showing roughly 8% growth per annum over the same period.

In part, this we believe divergence reflects the reality of global trade: While we typically think of emerging markets like China as being most exposed to US supply chains, the fact we have found many of the biggest EM firms don’t rely too much on sales to the US—they’ve got growing domestic consumption and exports to the rest of the world to tide them over—while companies in developed economies like Japan and Europe are often heavily dependent on US demand to drive growth. The kicker comes when one examines valuations: Despite expectations for nearly double the EPS growth in the coming years, MSCI EM stocks currently trade at a forward P/E of just 14x, compared to a multiple of over 21x for the MSCI World Index and a lofty 31x for the tech-heavy US NASDAQ composite.

Is there one more potential catalyst for further EM outperformance? The upcoming September FOMC. Some of the worst macro conditions for EM equities historically have been rising US rates and a strengthening dollar. In other words, just the conditions that have prevailed since pandemic-era inflation and the latest cycle of Fed tightening. With the US central bank under severe pressure to ease from the White House, tamer-than-expected inflation, and a softening labor market, traders put the probability of a September cut at 87%, with another four cuts priced in to occur over the next year—plenty of reason for investors to feel good about the future for EM stocks.

Disclosure: This material is for informational purposes only and should not be considered investment advice. The opinions contained herein are subject to change without notice. Indices cannot be invested in directly and are unmanaged.

Advisory services offered through Sowell Management, a Registered Investment Advisor. The views expressed represent the opinion of Sowell Management. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and non-proprietary sources that have not been independently verified for accuracy or completeness. While Sowell Management believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sowell Management’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. International investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles, or from economic or political instability in other nations. Past performance is not indicative of future results.